Simple methods-calculating client profitability

We know that advisory firms have built their success of the back of providing valued, quality advice to their clients.

Graeme Stewart

5 May 2021We are also aware that in the FAMR final report, a 2016 survey conducted on behalf of the Association of Professional Financial Advisers found that 69% of advisers said they had turned away potential clients over the previous 12 months. The most common reported cause for this was affordability, with 43% of advisers turning away clients stating the advice services offered would not have been economic given the circumstances of the client.

So, on one hand there is the “advice gap” where consumers cannot access the advice they want and, on the other, we have the rising costs of providing advice in our regulated environment.

One thing is for sure, as much as firms love to look after their clients, especially ones that have been loyal as the advisory firm has grown, if they cannot provide advice on a basis that is profitable to the firm, then they will need to think twice about providing advice.

So, how do firms go about balancing the desire to give great service and advice to clients, whilst working out if the cost to provide advice is sufficiently profitable to them to stay and grow their business?

Firstly, we will look at a simple process that a business owner can go through to discover just what level of income a client would have to generate in order to make them profitable and sustainable. We will then consider how any client deemed not to be profitable can continue to be supported to ensure that the firm meets their treating customers fairly obligations.

How much is enough?

In order to determine whether a client is profitable to a firm (or not) some consideration needs to be given to just how much it takes to provide advice to a new client and then, service an existing client who has an on-going relationship with the firm.

So firstly, let’s see what costs are involved in order to provide advice…

Whilst there is no perfect way to go about this, let’s look at a simple process that could be used in the first instance and, if further exploratory work was needed, the firm may then wish to consult their accountant to further identify costs and their allocation to each function of the business.

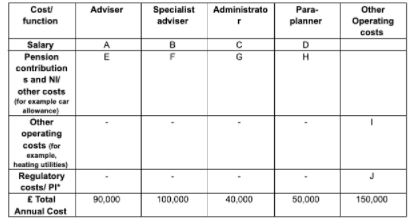

A simple model to identify costs:

* Firms could look at this in as much detail as they wanted, for example apportion the total costs over each function (allocating more PI cost to a specialist adviser) for example.

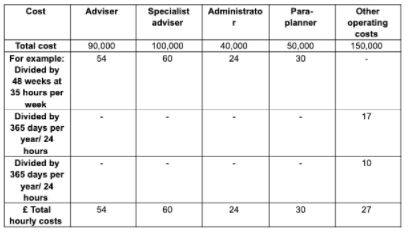

Having worked out an annual cost, we can now look at breaking this down into an hourly cost in order to work out costs in dealing with various client types.

So, we now have an hourly cost for each aspect of the business.

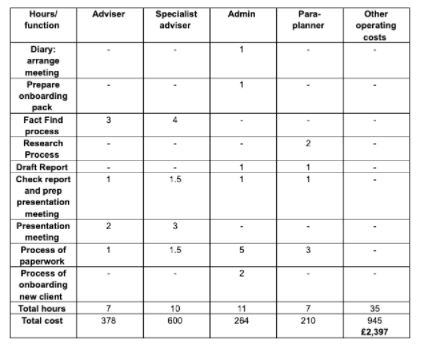

We now need to understand how much time is spent in servicing a client, a very simple model could be:

A new client

So, we have established, albeit roughly in this example, that for a new client the costs to provide advice is £2,397.

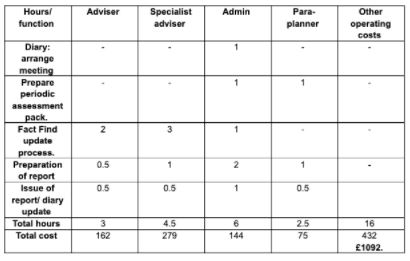

If we repeat the process again for an existing client:

An existing client on, for example, the “Gold” proposition

So, we have established that for an existing client, the cost to provide annual on-going advice to this client on the “Gold” service proposition is £1,092.

Of course, these figures don’t identify clients, who require additional support, perhaps through their on-going queries and requests for assistance in completing things like tax returns, but it provides a floor level where, if the fees generated by the client are less than £1,092, then they are likely to be an unprofitable client.

It is also worth doing the same exercise for each proposition the firm has in order to identify all potentially unprofitable clients within the entire client bank.

What happens now?

A careful client-by-client review is now required.

Some clients, who have been identified as unprofitable, may be clients that:

- Refer other profitable clients or have the potential to refer profitable clients.

- Are closely connected with profitable clients.

- Will become profitable over time, or after certain expected events.

There are now many different options as to how a firm may want to proceed.

Options

Existing Proposition Costs

This is a delicate matter, and will need to be handled with great care, but firms may find that clients are willing to pay an additional fee to continue to receive the same, valued services and advice from the firm via a top up fee, confirmed with a fee agreement. This is certainly the win-win situation, where the clients continue as they and become profitable for the firm itself.

Alternatively, the firm can review the costs associated with each proposition. If the proposition costs can be further broken down, reviewed and then reduced through greater efficiencies in the advice process, it may be that more clients can now be considered profitable.

Finally, the overall cost of the existing proposition could be increased, but careful consideration of this has to be made as to what the impact will be on the clients themselves and the on-going suitability of the advice. No firm is going to increase their charges without very careful thought of this.

Swap Propositions

For those clients who have been identified as unprofitable in the “Gold” service, could, if it is suitable for them, be placed in an alternative, lower cost proposition. That way the client knows they will receive the services that are suitable for them, albeit at a reduced level, and the firm can continue to provide the on-going advice and services at a profitable level.

Create new propositions

If the firm has identified a number of clients who are not currently profitable, the firm could construct a new, alternative proposition to meet this segment of their client bank needs. This would fit in somewhere between the existing propositions, costed using the methods above, to ensure that a suitable on-going proposition could be offered at a cost that is profitable to provide and would still be a valued service that clients would want to partake in.

Of course, once this new proposition is up and running, it is possible that this could be used as a way to attract new clients, potentially reducing the advice gap.

Move to a transactional arrangement

Clients who are not profitable to a firm could be moved to a transactional basis only. This would also need to be carefully explained to a client so that they fully understand that they will no longer receive a pro-active advice service, rather that the firm will only re-act to a client query for which the client would pay for services on a PAYG basis. Whilst the firm would have to cancel all on-going income from providers, they could still keep in touch with these clients, through newsletters etc. encouraging them not to lose touch with the firm and to return for advice as required.

Sell the clients?

One further option would be to consider whether the identified group of clients could be sold to a different firm with a suitable proposition. This is perhaps a complex alternative, and possibly a last resort, but the firm could at least re-assure themselves that the clients they have cared for in the past would be well looked after in the future.

Conclusion

As advisory costs appear to rise each year advisers, more than ever, need to be aware of which of their clients may actually be impacting on their firm’s profitability, so that they can try to provide them with the on-going support they value.

Whilst the methods to determine profitability, described above, may be simple, they should allow firms to delve a little deeper into their business to ensure that the hard work needed to provide great financial advice is at least a profitable venture for them, and allows a firm to determine where to focus their efforts.